Weekly Global Macro Update April 3rd 2018 "Q1 2018 Insight and More"

It's supposed to be springtime, but it sure doesn't feel like it, at least not in Chicago. We chose the picture to the left as it is clearly representative of current state of nature and maybe representative of the overall state of financial markets as well. With Q1 over, the year started out in equity land partying like it was 1999, but then the tide turned and optimism turned into fear and the markets finally had a 5% down move, something that it hasn't seen in quite sometime. So where do we stand now?

Well college basketball is over and once again the Wildcats of Villanova are back on top, taking only a year reprieve from their last NCAA tournament crown from 2016. Baseball is back upon us, yet the weather in most of the Midwest and North-East is certainly not conducive for such activity as Spring seems to be put on hold. Seems as if the Astros, Dodgers and Indians are the early favorites, although in Chicago the Northside is as always, a perpetual optimist, where on the Southside, the prospects are quite improved, as for our Bulls and Hawks, well we’ve certainly seen better days, it was a good run though boys!

So, with the first quarter out of the way it seems as if the tone has certainly been set. The Fed has continued its rate hiking path and volatility has disrupted the 8 year long near linear equity climb in its tracks. We have noted that interest rates are the thorn in the equities side as the mathematics of our debt is most certainly going to become more and more a burden, not just for us, but the rest of the world as well. Short term interest rates have been bludgeoned and rightfully so given the path or our hawkish FED. They bought a decade and it is no doubt just making room so that it can hit the #QE4EVR button once again. What is also scary is the thought of a UBI or Universal Basic Income that we have been hearing as of late. This is a dangerous Socialistic path and one by which we would should definitely find alternatives to, nevertheless the drumbeats are getting louder and all the talk of AI and Robots replacing our workforce is adding to the hysteria.

The first quarter has also brought President Trump continuous cannon fodder for his Tweet storms and no industry, no celebrity, no corporation is off limits. As we have stated before, POTUS has a plan and he is merely trying to stay the course and for those that don’t think the wall is going up, rest assure the first course of actions set by the recently passed omnibus bill is for more military spending, which will be directed to sending troops to the southern border. Then once the troops are there the Army Corps of Engineers will be instructed to sign, seal and deliver said wall. Whether the left wants to fall over and complain, simply doesn’t matter, the bottom line is Americans want it and globalist’s hate him for it.

Ok enough jargon let's get to a few recent items of note:

The biggest development this week was the publication via the NY Fed of the new Secured Overnight Financing Rate or SOFR. We expect the adoption to be widespread and as far as we are concerned it will replace the LIBOR rate because the mass manipulation and bad Karma that comes with all the exposed LIBOR rigging means the powers that be need to shift the narrative to a new entrant and thus SOFR and its near $trillion in overnight usage. Link to a Reuters piece can be found Here

Walmart Inc. is holding preliminary discussions to buy US health insurer Humana Inc. No guarantee yet however, on a merger or partnership. Walmart, which has seen its profits decline by 30% over the past 3 years, to $10.5 Billion is on the hunt for growth. This diversification makes sense given their declining profits and will put them into the thick of the healthcare race, where mergers and acquisitions remain at a dizzying pace. Aetna the insurance giant was bought by CVS Health late last year for $69 Billion. Earlier this year Express Scripts a pharmacy benefits manager was bought by Cigna for $54 Billion.

The Walmart-Humana deal makes so much sense in the growing field of healthcare and in the shrinking field of providers. Walmart is certainly banking on leveraging its already dominating grocery business and in our opinion this just makes perfect sense. Why not offer your customers two of the very basic necessities in life, food and healthcare, in fact Walmart’s future no doubt holds a blockchain, decentralized ICO and issuing their own tokens for their users which would benefit immensely from the seamless integration of providing a blockchain token that would enable Walmart shoppers to buy groceries and healthcare. We suppose the next link in the Walmart chain would be affordable housing mortgages, then their dominance would certainly be sealed.

Barclays was slapped with a $2B fine this week in civil penalties tied to US Dept of Justice claims for selling fraudulent mortgage securities during the financial crisis. So, nobody goes to jail and they get a slap on the wrist, $2Bln what a joke, they made that and 10x more no doubt. Once again, if the bad actors don’t pay a legitimate penalty price, then the mantra that “crime does indeed pay”, still holds true.

The financial market exchange giant CME Group this week purchased NEX Group PLC for $5.4 Billion. NEX owns BrokerTec, the largest electronic trading platform for U.S. Treasuries. We are optimistic that CME lobbyists will go to Washington to change Rule 42.10 which restricts participation to only those entities with $45 million or more. Chicago prop groups were at one time the dominant players in this sector but of course FED oversight and regulation was fully intended to keep participation to a minimum. (WSJ)

Also, out this week was more bad news for Tesla, as they issued a recall for 123k Model S sedans built before April 2016. The recall is to retrofit the power steering component. Their bonds and equity have certainly both been victimized lately.

News out this week that AIG paid $67.3 Million to its CEO’s last year, the figure which included CEO’s Peter Hancock who resigned in March. Remember AIG through the Federal Reserve’s Maiden Lane II and III bailout package 9 years ago, gave AIG $185 Billion so it wouldn’t fail, or so Goldman wouldn’t fail, or so none of the banks would fail, you choose…ahh, how nice to be in the club, wouldn’t it be great if the commoner could get a juicy bailout? Remember AIG paid out soon after receiving that bailout $165 Million in bonuses, must be nice right?

The Senate Judiciary Comm. Asked Facebook’s Mark Zuckerberg to appear at an April 10thhearing on data privacy. Facebook has been in the hot seat for the last few weeks as it was revealed that it sold tens of millions of user’s data to Cambridge Analytica. Now we all know the numbers are much larger and the abuses far more reaching, the scary thing is nobody really seems to care.

President Trumps tweet targets last week included in its sights once again Amazon. It has been known POTUS has been an outspoken advocate against Amazon’s role in everyday life. He has been especially brazen, as to the governments role in assisting Amazon deliver packages, as well as the limited amount of taxation the company seems to ultimately pay. We expect this rhetoric to continue, especially given the trajectory of the U.S. debt pile that someone will have to finance.

Spotify Technology SA the Swedish music streamer is set to price a direct listing this week on the NYSE. Its set to open near above a $130 price target. As of this writing, Citadel has priced the opening trade at $165.90, well above the $132 reference price set by the NYSE. This was not an IPO, but a direct listing, which saved Spotify millions in fees. It was last seen trading near $149 which would put the market cap around $33 Billion. With stiff competition in this land we will expect some volatility in pricing over the near term and for those looking to get in, please do your research!

One decent highlight this quarter and after jumping 35%, Cocoa was by far the best performing asset out there, but it did see some profit taking today as denoted in this chart from Finviz.com:

Some notable Q1 2018 results on the upside were:

Corn was up 10.55%

NYMEX Crude was up 7.48%

The NASDAQ Composite was up by 2.89%

Some notable downside returns were:

US 5-year yields lost 18% in terms of basis points rise

The SP500 Index was lower by 1.23%

Comex Copper was down 7.94%

The FTSE 100 lost 8.21%

Sugar lost 18.54%

Lean Hogs lost 20.24% although they are up around 8% to start the quarter!

Ok let’s get to some technical charts:

The DJIA has hit its 200 day Moving Average and this is not good for equity bulls if this level is closed below. This should continue to attract reactionary buyers but the exit visas will be limited if it breaks, so keep a close eye on it:

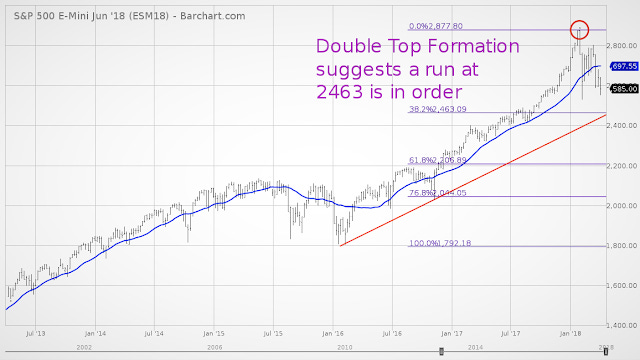

The SP500 future continues to target initially the 38.2 Fib and the trendline which converge now at 2463. To say this is just the first step in a long correction process is an understatement. We are beginning to look at the SP500 like its 2007 all over again:

When we observe the ETF QQQ 152.75 is huge and should see buyers come in at that level, but how long it lasts is anyone’s guess:

The U.S. Treasury market may be showing signs of max yield rise given the volatility increase in the global equity markets. The 30-year treasury bond future is approaching the 200-week moving average which if broken may set in motion some trend following CTA’s and those caught short will be taken out to the woodshed:

Ok that does it for this week, we will continue to monitor the markets and bring you only the things we think represent the real potential to drive markets in significant ways. We continue to believe the #BTFD is over and that real managers are going to have to adjust their free money buy only algorithms. We expect many a manager to show their true colors and not be able to handle the coming changes as far too many have been lulled to sleep. Oh, before we go, and something that we touched on some letters ago, Jeff Gundlach of Doubleline was on the wires this week again, saying how Bitcoin may be leading the movements in the equity markets. “it’s all tied together, obviously,” Gundlach said. (Reuters) We took a lot of flak months ago when we even suggested this correlation, so we are glad an astute and formidable player as Mr. G, feels the same way, that’s why we respect him so much. He isn’t afraid to swim against the current.

Anyway, we saw this picture again, and we can’t help but smile and think the Mnuch and his trophy picked up some new toilet paper for their Manhattan penthouse!

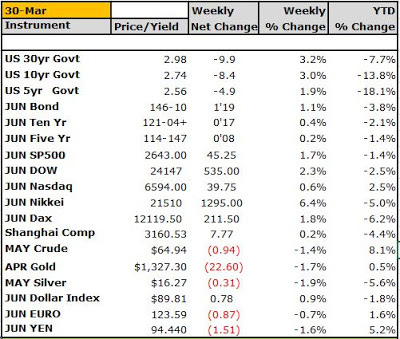

Ok we leave you with the Settlements which actually are of Thursday March 29th per the Good Friday observance. Cheers!