Weekly Global Macro Update April 10th 2018 "No Room To Maneuver"

We have a lot to get into this week, but let’s begin with a POTUS tweet which in our opinion sums up any trade war provocation worries some of you may have. Although, most might think President Trump's approach is a bit boorish and harsh, we view it more from the lens of hard truth, which sometimes strikes a better chord when presented non-sugar coated:

So, we will take Trump for face value and say he is committed to the #MAGA. We have spoken at length about this and he is following thru whether the globe likes it or not, good or bad, repercussions notwithstanding. In a nut shell Trump is playing a game of chicken with China and given the fact they have about 1 billion more people to feed and who knows how much actual debt, local and shadow to combat with. We would also like to point out the fact that we made light in our past letter that the new omnibus bill made provisions for increased military spending for the border and what did we see this week?

Arizona and Texas National Guard are sending 400 members to the southern border. We can only feel the next step will be construction which we also believe is within the provisions of the new omnibus bill. Time will tell, but things are leaning that way.

We read further this week China has boycott buying US debt, hmm let’s just see how long that lasts. It makes it a bit tougher to peg a currency if you’re not intervening and we feel this bluff won’t last long both from a fundamental viewpoint and certainly a domestic stability front.

As far as China and their massive credit financing schemes, ghost city infrastructures, WMPs etc, we think the picture to the left best describes their ability to maneuver.

Just to put this into perspective in a matter of just 2 decades, the PBOC has grown its balance sheet from $40 Billion to over $4 Trillion. There is a cost to that type of hyper growth and unfortunately money is debt and thus a government must also pay the interest costs associated with such growth and in China’s case exports are the driver and when someone like the U.S. pulls a protectionist move, its like an artery that gets clogged, you either fix it or the problem kills you, so will see where this all goes.

We won’t go any deeper than that, but I think Trump knows the “America First” agenda is catching many of our partners by surprise and this is the best way to force change.

A few items of note this past week:

The BLS Payroll report was out last Friday and it posted a huge miss adding only 103k jobs with an expectation of 185k. Labor participation is stuck near 63% which is where its been the last few years. The unemployment rate stood still at 4.1%

S&P500 earnings are expected to rise 18.4% in Q1 according to consensus estimates, driven largely by the huge Trump tax cut. This would also be the largest profit rise since Q1 2011

Chair Powell was in Chicago this week and suggested that “there was no hurry to pick up the pace of rate increases and described the current course as prudent” (WSJ)

ICE to Buy Chicago Stock Exchange, WSJ reported estimate price of around $70 million

SP500 lost 58 pts, the DJIA lost 572 and the NASDAQ lost 161 Friday

US deploys Truman Carrier Strike Group And 7 warships with Cruise Missiles to Mediterranean

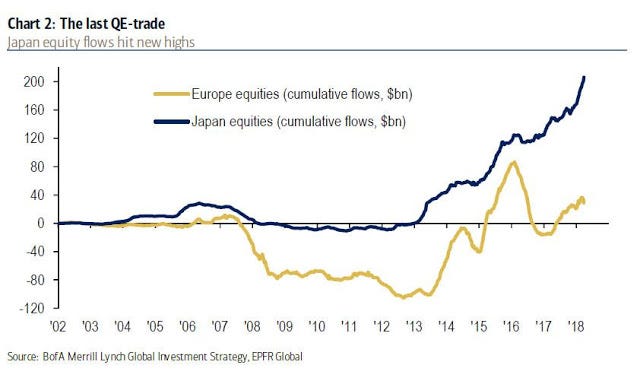

BofA had a great article out this week noting some very interesting points. The first thing that stood out is the fact that central bank policy is driving equity flows and this next chart clearly displays this, as both Europe and to a better extent Japan equity inflow continue:

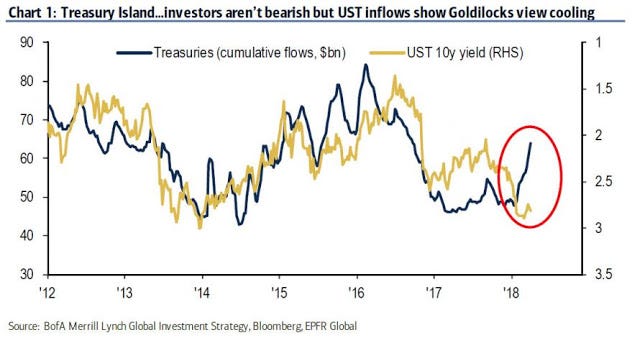

The second thing we want to point out is their treasury cumulative chart flows which may be signaling and this is our opinion a delayed response for interest rates to fall not rise given the cumulative flows:

Also, out this week, John Mauldin put out a great piece entitled “Assumptions Equal Problems.” He outlines the fact that the CBO makes certain projections and these projections are full of assumptions, but in reality, the government makes rash decisions. These decisions have far and wide repercussions and they certainly change the future in varying ways, in unexpected ways. Mauldin pointed out the 2001 surplus projections and how things can change very quickly and most often on the heels of adverse shocks to the overall economy. We touched on the CBO projections a bit last week and stated that its forecast is highly improbable given that no recession was on their radar. As that point, in of itself is highly unrealistic, then we must assume that the rest of the report just like the 2001 projection for budget surpluses was also highly unrealistic. Nevertheless, we know to take governmental agency reports as a supplement not as a guide to our future assumptions.

Anyway, as of this writing and considering the timing of the Facebook Senate hearings, we found time to highlight a few interactions. We knew it was just a Dog and Pony show, given the fact that the Zuck donates to around 85% of those Senators in attendance. We highlight a few points with some of our own attributes here for your amusement:

When asked whether or not Facebook uses the mobile device microphone to record audio, the face behind Zuck, which is most certainly legal counsel is priceless:

Anyway, usually these types of hearings aren’t negative for an equity and in fact the markets overall are doing quite well as of this writing. So, take this as nothing more than an informal informational hearing. As to Facebook being held responsible, we highly doubt it. What this should point out to people is the fact that ANYTHING AND EVERYTHING that you put on the internet is open for download, by ANYONE GOOD OR BAD. However, and a big however is whether or not this should be regulated, whether or not Facebook is using censorship, whether or not free speech is free. This opens Pandora’s box in terms of rights toward one’s data and we expect this to be an ongoing process. We would just like to say, if you don’t want your data out there, don’t put it out there, period. Power is on the individual, nobody is telling you to go get a Facebook, Instagram, Snapchat etc. So, no complaining, just action please.

As for technical charts and thank you to KeystoneChartsInc, let’s check some out. First up the SP500 futures, Keystone points out the clear trading range of 2584 to 2655 area:

The DJIA is still bearish below descending trendline at 24689:

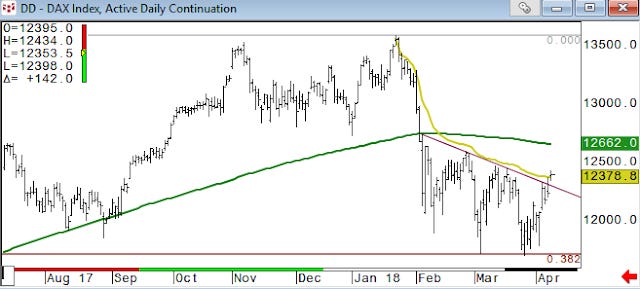

As we touched upon earlier the German DAX equity market has seen clear support since the US equity markets have been under fire, here is a chart we aren’t sure if this will pull US equity markets higher, but it is certainly on our radar:

This next chart is very specialized and one we thank Dave at Keystone for providing. Basically, this is a long SP500 combined with a long 30yr US bond and what it will show is since the breakdown of a very long trend channel we have been in a sideways consolidation mode and we respect this chart to provide a clear breakout if and when:

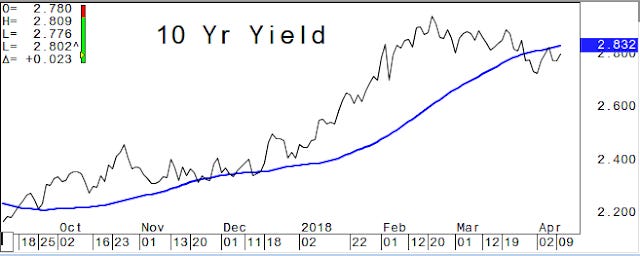

As far as the US 10yr yield chart, you can see the 2.83% level is very important and lower rates is the course if the yield continues on below this important level:

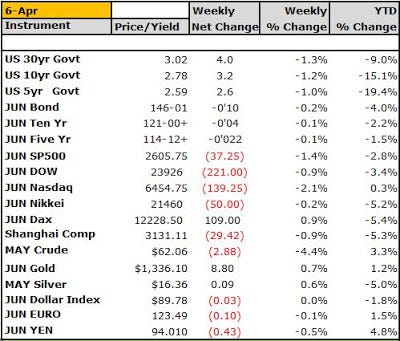

In conclusion we leave you with the weekly settles for trade date ending Friday April 6th. As you can see US 10yr yields seem to be stuck between 2.75 and 2.85% for now. US equity markets lost some ground last week and the NASDAQ is breakeven on the year. Crude fell back a bit last week, but with renewed Mideast tensions we are certain this will give it short term support and gain further traction if this is just the beginning of a deeper US presence in the region. Let’s not get confused, there is a lot of noise, Facebook, Mideast tensions, Tariffs etc., but in reality, the overall market moves are based on large fund flows and despite the markets large moves lately, we feel no clear path exists. We feel the equity markets have technically been under fire and the bond markets are in stand still mode. This environment is a tough trade because the overall market’s direction or trend is undefined. Many are calling a top, many are calling rates to rise and on the flip side, time is telling us this is nothing more than a range and the future is uncertain.

So, to all our traders out there, stay quick and nimble and realize that nothing is set in stone, but we hope we provide information that gives you something to cut your teeth on, cheers!

DISCLAIMER: For Educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures nor an endorsement for the purchase and sale of ICOs or Cryptocurrency and should not be construed as such. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Mike Agne of Agne Asset Management LLC (AAM) and owner of www.econemotions.com and The CryptoCorner Newsletter, that you will profit or that losses can or will be limited in any manner whatsoever. The CryptoCorner logo and name is the sole right and property of (AAM). Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, (AAM) makes no warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.

DO NOT COPY OR FORWARD INTELLECTUAL PROPERTY WITHOUT PRIOR WRITTEN CONSENT AND OR APPROVAL