What Happens To Underfunded Pensions if Markets Move Lower?

Before we jump into market action, we just have to comment about the ongoing spectacle in congress. Just to recap our readers, and without any political bias, let’s just get to the facts. There have been ongoing investigations into the Russian collusion in the 2016 election, whether or not that collusion was done for the pro Trump crowd or pro Hillary crowd remains to be seen, we don’t really care. What we do care about is the fact that members of our intelligence community were using private emails and servers and discussing extreme bias while investigating and some very curious events ensued. Now for those that aren’t in the know about the ongoing deep-state vs the current administration battle, it has now moved to the congressional oversight committees, where this week a one Peter Strzok a former counterintelligence operative and current FBI agent was testifying before congress.

We urge you to watch what is going on here and we know that 99.8 % of the American population would never watch this, (truly sad by the way) but we highly suggest you see what your country is up against. Just to be clear we aren’t taking a political bias here, but rather we want you to be in the know. This is just the beginning of this battle the story line is long and goes very deep and it will have a major impact on our markets, this we are most certain of. These hearings are just the beginning and they will be at the forefront for quite some time. We exposed some of this for you a few letters back when we talked about the “Q” movement. Now our editor might not be happy, but we believe you should be informed and it is our job to inform you, anyways this Peter Strzok case is somewhat relative to the financial industry as his wife works for the SEC, promoted curiously in 2016 to associate director in fact. Anyway, we urge you watch this and think long and hard what is about to go down, the full video can be found here at, PStrzokCongressTestimony What is crazy is how the Democrats protect this guy, obviously just to stay within their party lines, but really? Did you read his text messages? Morality and Ethics doesn’t have boundaries, isn’t limited in scope, its absolute, sorry.

Speaking of Trump, collusion, Russia, this week is historic as Trump is set to meet Putin in Helsinki. We know the left will be pushing the Russian/Trump puppet BS, but the focus should be upon diplomacy and peace and any talk otherwise is plain stupid. We are sick and tired of moronic inclinations that Russia is controlling anything, the United States is the most powerful country in the world and Russia -US relations need to be in balance. Any argument against diplomacy is an argument for aggression and adversarial confrontation, who benefits from that? What is the price of peace? Which would you rather have peace or war? These really are simple questions and if you can’t answer those clearly, then you are certainly lost and there isn’t any hope. Anyway, the meeting is historic and we here would rather put our trust in diplomacy rather than in the hands of any aggression.

Global equity markets continued to advance last week. Last week’s update noted the importance of closing the week above the all-important 2750 level in the EMINI SP500 Sept contract. We knew this level was huge considering the close below on June 29th sent the contract below our 7-week moving average and was on the cusp of losing further ground. But all tariff worries aside, all geopolitical NATO posturing aside, the equity markets continued their advance on the tailwinds of massive continued corporate buybacks. Before we get into the markets lets dig into a few notable names from last week. Wells Fargo saw Q2 profits sink 11% on weakness in their main business units as well as ongoing costs related to their terrible mismanagement of corporate integrity. Their shares fell 1.2% to $55.36 on Friday. On the flipside PNC Financial Services Group saw profits jump 24% to $1.35 billion. Shares rose 33 cents to $138.42. JPMorgan and Citigroup also posted double digit profits as borrowing rose. So, it seems the flat yield curve hasn’t shown up in the earnings. (yet)

American Airlines group lowered its Q2 revenue outlook, noting rising fuel charges. AAL lost 8% on the news from Wednesday and closed Friday at $37.12 up 79 cents. Computer Associates (CA) spiked 19% last week as it agreed to a buyout from Broadcom Inc. Broadcom is offering $44.50 per share. The deal is valued at $18.9 billion. Papa Johns popped 11% last week as founder John Schnatter resigned as chairman, can you say insert pizza foot into mouth please, we can’t imagine the PR nightmare, for some reason a one Paula Deen comes to mind…

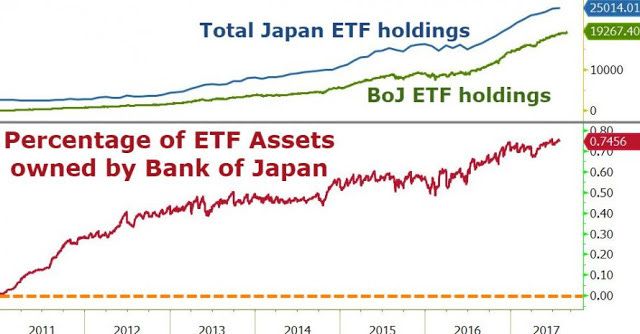

We also read a good note from John Mauldin last week, one thing he pointed out was this, “A new report by the American Legislative Exchange Council (ALEC) shows the unfunded liabilities of state and local pension plans jumped $433 billion in the last year to more than $6 trillion.” We point this out because if the SP500 return was 22% last year and the NASDAQ was 27% yet the unfunded liabilities grew some 38% what will happen when the market has a down year? These are truly scary figures, as we have said time and time again, update after update, that the mathematics will eventually destroy all of these illusions. Using debt to supplant savings for organic growth is governed by the exponential laws of diminishing returns, or in simpler terms as time moves to the right, it will take more and more debt to produce an equalized amount of growth. The longer that persists, the larger the problem gets and it never truly goes away, but it dies in spectacular fashion, unfortunately!As long as the pension funds and central banks are willing buyers, either directly or indirectly through stealth operations then the day of reckoning keeps getting pushed out. Speaking of central bank and pension fund buying, and the correlation as to why markets never fall, we present this chart from Zhedge:

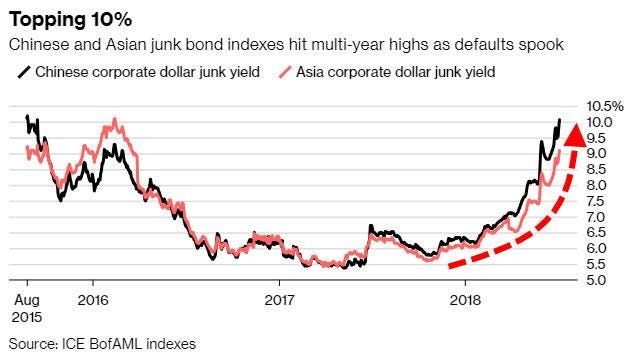

Staying in Asia, the next chart is troubling, we touched on Chinese Shadow Banking last week, and we have seen noticeable contractions in the data there. Considering this tightened environment, it is no surprise that junk bond indexes in China and Asia are climbing:

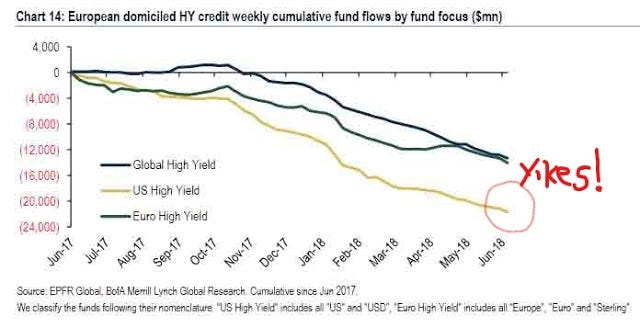

We also saw an interesting chart from our Zhedge friends, this time displaying the Europe and EM equity fund flows, which have plummeted to multi-year lows. The contrarian in us can’t help but think a hefty global pension and SWF roll-tack maneuver may be upon us. For those that aren’t into sailing its in reference to sailors moving in unison to one side of the boat while turning through the wind, using the weight of the crew to assist. In the markets case, it’s getting everyone on the same side and then take the trade square in their face. Anyway, and considering the huge underperformance of the DAX this year compared to its U.S. counterparts. The intuition in us senses a change may be upon us as everyone’s on one side of this boat. As far as looking at an overall European picture of funds in regards to the high yield market, this chart clearly shows the breakdown since late 2017:

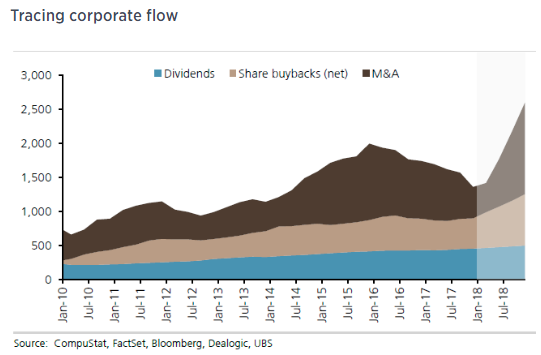

Ok just to be fair there is a flipside to all of this selling, right, zero sum games after all. Ok so in order to save the day, the buying can simply be summed by taking all the buybacks, all the dividends and even further all the share smashing M&A activity. So, I guess it’s a function of simple supply demand, remove shares, price increases nominally:

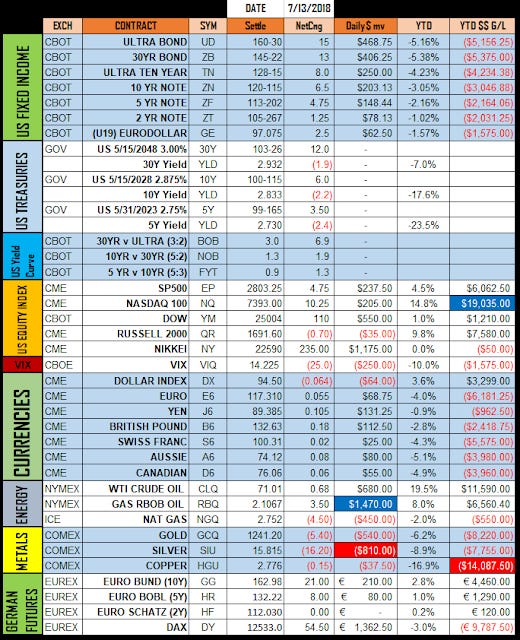

Ok let’s take a look at last Friday’s settlements prices:

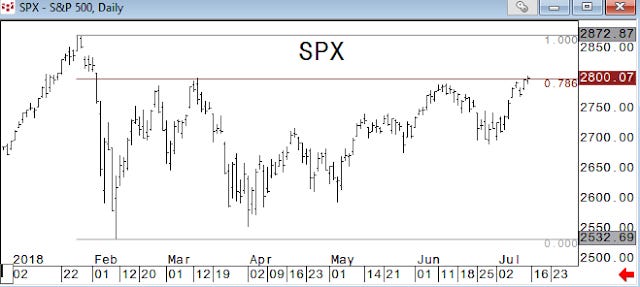

We will continue to monitor this asset allocation of EM vs DM and more precisely the Nikkei and DAX vs their US counterparts. I find it very curious that the US fixed income has held up so well with equities rising. In particular both the US govt 30-yr and 10-yr auctions went well. The yield curve continues to flatten and option gamma seems to be picking up in the short rates, so something might give here, will see. Let’s take a look at some SP500 charts (keystone charts inc), the Sep Future looks heavy under 2814 and that provides formidable resistance for now:

The SPY is also providing similar resistance near the 279.70 area:

As far as the SPX this 2800 level seems obvious for the bulls to maintain or lose mojo:

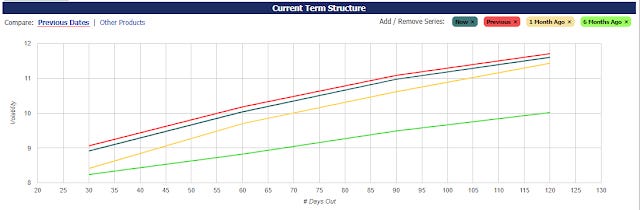

As far as the change in the Term Structure of the SP VIX we have this chart, obviously 6 months ago VIX was 40% cheaper:

Moving onto crypto land we have some key developments,“The U.S. Securities and Exchange Commission and the Financial Industry Regulatory Authority approved Coinbase’s purchase of Keystone Capital Corp., Venovate Marketplace Inc. and Digital Wealth LLC, a company spokesman said Monday. The acquisitions enable the firm to offer so-called security tokens, and also place the businesses under federal oversight. Coinbase has primarily been regulated by a patchwork of state authorities.” The move provides Coinbase licenses to operate as a broker dealer, an alternative trading system and a registered investment adviser, the San Francisco-based company said in June. Alternative trading systems operate outside traditional public stock exchanges. (Zerohedge)

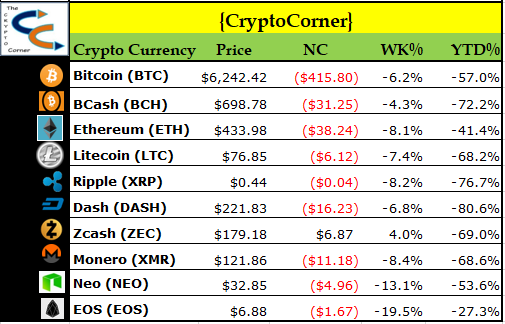

We can only figure that Coinbase, originally backed by a few US institutions and is seemingly in favor with the IRS, is now prepared to be the house or exchange for US crypto currency participants. For all those that think buying and selling Crypto is anonymous, think again, each and every transaction, purchase, transfer will now be logged and traced, i.e. PAY YOUR TAXES! As far as last Friday’s crypto settles.

This week has the latest PPI and CPI reports, fodder for some inflation/deflation debates as well as a slew of earnings which can be found HERECongrats to this weekend’s big winner, France at the World Cup. However, we think the real winner was actually Juventus as they welcomed their newest team member Cristiano Ronaldo from Real Madrid. Juve has a long-celebrated history much like Real Madrid. We studied Real Madrid in biz school and we were quite impressed with their president Florentino Perez. He truly turned soccer into a global enterprise by merging modern day business tactics and marketing with a globally embraced sport for all ages. Perhaps Mr. Agnelli of Juve hopes Ronaldo will increase, not just victories, but revenues, we would bet that is a solid lock on both fronts! Congrats to Novak Djokovic and Angelique Kerber on their Wimbledon victories. Ok, that does it, we hope you have a great week of trading and investing, thank you for reading our report.

DISCLAIMER: For Educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures nor an endorsement for the purchase and sale of an ICO, Cryptocurrency or any digital asset and should not be construed as such. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Mike Agne owner of Magnelibra Capital Advisors LLC (MCA) and the website blog, which can be found at www.econemotions.com. All rights are reserved and encompass MCA and The Crypto Corner Newsletter, we will never claim that you will profit or that losses can or will be limited in any manner whatsoever. The Crypto Corner logo and name is the sole right and property of (MCA). Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, (MCA) makes no warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed. DO NOT COPY OR FORWARD INTELLECTUAL PROPERTY WITHOUT PRIOR WRITTEN CONSENT AND OR APPROVAL