Good morning everyone, I hope you guys are having a great week so far and welcome to another edition of the Magnelibra Markets Podcast. Today’s episode #56 is entitled “Where Are We At”

Quick Disclaimer: The following podcast is for educational purposes only. This is not a solicitation to buy or sell commodity futures or options. The risk of trading securities, futures and options can be substantial and may not be appropriate for all listeners.

Ok guys I entitled today’s podcast Where are we at, for a very good reason. All to often we get caught up in the markets current movements and forget to look at the bigger picture. Obviously many traders, especially short term or algo types could care less about this stuff, however long term investors, which make up the majority of investors it does indeed matter.

It is obvious now that the new incoming administration is going to make some serious big league changes and some may discount or underestimate the ramifications of what is truly going on. A lot of what the new administration talks about are changes that will greatly impact many industries and will force sweeping change across many companies that have come to rely on the US Govt as their major source of revenue. It is apparent that Elon Musk and Vivek Ramaswamy are at the forefront of these sweeping changes and that provides us with great insight because they undoubtedly have “eliminating waste” as their number one priority. So in the coming months it will help us all by reviewing major corps that have the US govt as a client and seeing exactly how much of their bottom line may be affected by what is to come.

Secondly, we know the new administration has been very vocal on the topic of implementing tariffs. We know that word is taboo around many circles, but it doesn’t matter what many think, only what the administration thinks. That is the reality and there is no doubt in our minds, that tariffs are at the forefront of improving the domestic pricing power of our goods and services sector. Yes there will be unforeseen collateral damage, but that goes with the territory. Rest assure geopolitically that this will have major ramifications.

Thirdly on that geopolitical front, the global leaders will once again have their tails between their legs because they know what kind of tolerance the new administration will have, absolute zero. So with that expect an end to many of the on going conflicts because the new administration has a binary construct, a kind of F around and Find out mentality and that type of demeanor causes many to rethink their current endeavors.

Not all is so scary however we feel there will be many positives that will come out of this new transitional form of governance. We are pro less regulation and we know that the regulatory landscape shackles many corporations both large and small. Any sweeping overhaul of this will be welcomed by all and this combined with changing the tax environment to become more favorable, well that may be just enough to offset any exogenous unknowns that will arise from all the other changes.

Also we have to talk about the future of anti trusts. I feel that the new administration will be very hard on companies that have a strong hold that stifles innovation and competition, this is also a key topic and will see just how far the administration will go to take on some of the very large companies using their prowess to effectively eliminate any and all competition.

Furthermore we know changes will be coming in regards to the Federal Reserve, we already heard in the last pressor that JPowell, will not step down if the new administration wants him out, well in effect he is correct, only congress can remove him, but who knows, the precedent has already been set, we know the new administration feels that the FOMC could do more and this battle will be epic. We also know that the new administration is a fan of Dr. Ron Paul. For those of you that don’t know he is a big opponent of the Federal Reserve and we often loved his questioning of Fed Chairmen during the congressional meetings! So all in all we know things are rapidly changing!

Now as to the overall affects of the markets. One thing is clear, a lot of major investors have taken the election results and have bid the US Dollar. This is most likely causing major pain toward any short dollar denominated debt holders out there. Their local currencies weakening it makes their ability to convert their currency to pay back US debt a whole lot more expensive. Yea Yea, for years we heard and have debunked the “US Dollar is dead” cheerleaders, the reality is, so many are short that the scramble to accumulate dollars will be an epic squeeze like no other and that truly will have major global implications!

Take a look at the US Dollar chart straight up since the end of September, currently up +6.5% since then, now running into the last major resistance before we start to see the real dollar shorts panic:

Alright, so that defines where we are at, now lets look at the tecnicals in some of the markets we cover. First up the Dec Nasdaq. For some reason we feel a weekly close under 21000 will be very bearish, because we have the post election run up and now any stall out may see some mechanicals step in to press the new longs. Nothing is ever this easy and thus we have marked this 21k area before as a major hurdle area and target so bulls be careful below this area if the weekly settles under here:

Same thing goes and is nicely tied with the Dec. SP500 and the 6k area:

No analog is that good where we get 2 markets with major points of pivot lining up nicely like 21k and 6k, but that is what we have, for the bears, they hope for the weekly close below, for the bulls, that is your key level to defend!

Another market that has been pummeled by the stronger US Dollar is the Dec. Gold now down -8.1% off its highs trading $2573 -4.5% on the week. Target support area isn’t till $2493. Any gold bulls are usually longer termers, but for you traders, rest assure sellers are in control here and that target level of support is still some $80 away:

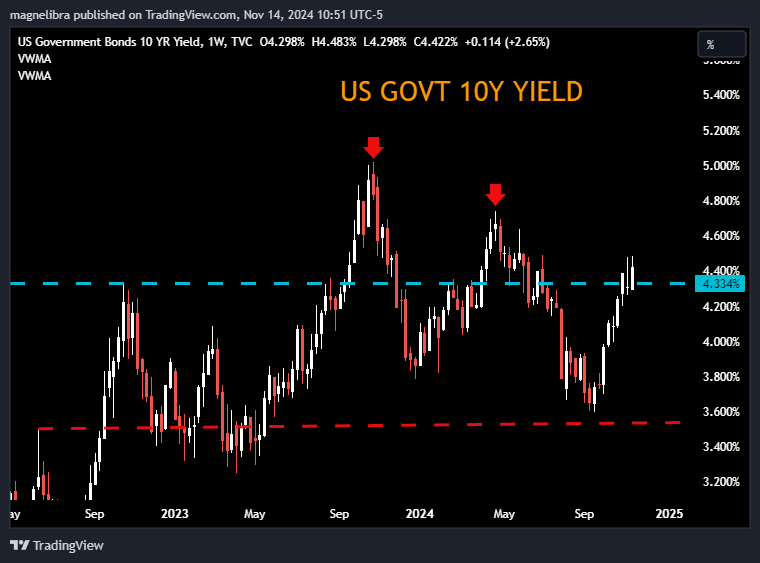

In US bond land we can see that the longer end continues to weaken (rise in yield) and why not, we should suspect that all the eyes are on the short end where the FOMC can influence. So with that we like to look at the US Govt 10yr yields which since late September have been in a nice correlation with the US dollar as the Dollar strengthened as yields rose:

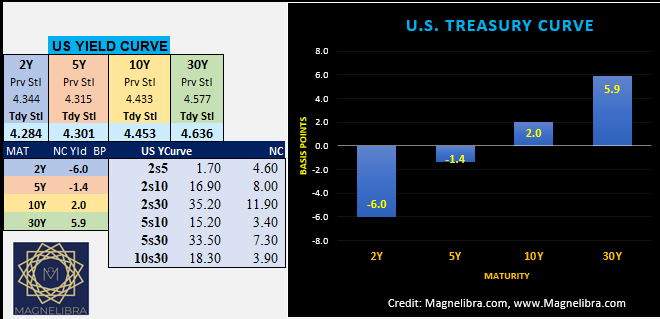

The 4.34% area is our pivot and the Bond Bears seem to have control for now, so this is the key level to watch! We know the FOMC will have to continue cutting rates and we have outlined that thesis many times. There is too much at risk for a US Treasury paying $1Tn plus in interest and not to mention the wall of corporate debt due ($7Tn plus) in the next 2 years. All of it requires rates to move lower and that will be our expected path expectation as well. We can see that the long end continues to rise while the short end falls which is evident in yesterday’s bond yield curve as the 30Y +5.9bp while the 2Y -6.0bp:

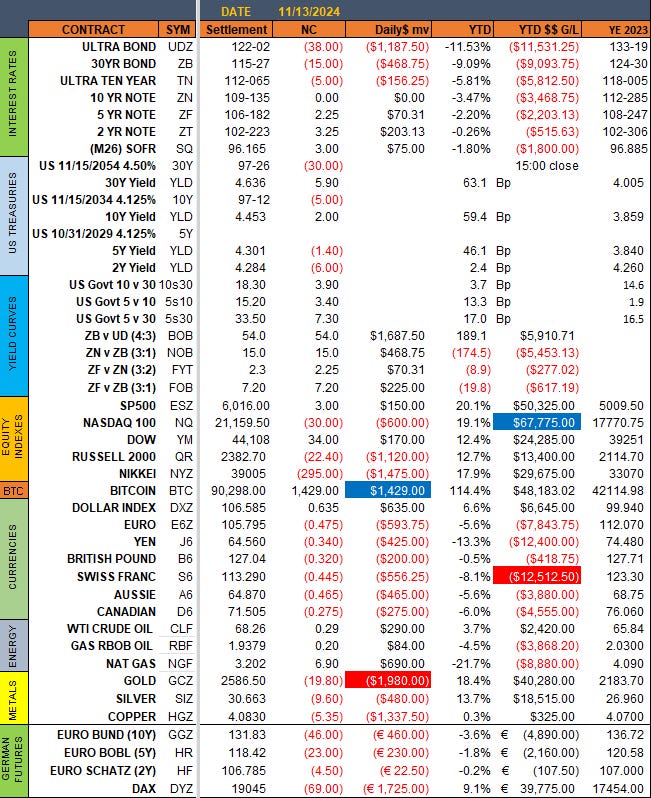

Ok onto this mornings PPI report +0.2% MoM as expected but YoY +2.4% exp +2.3%. We don’t take any single print other than that, with portfolio management costs adding to the final demand services up tick!

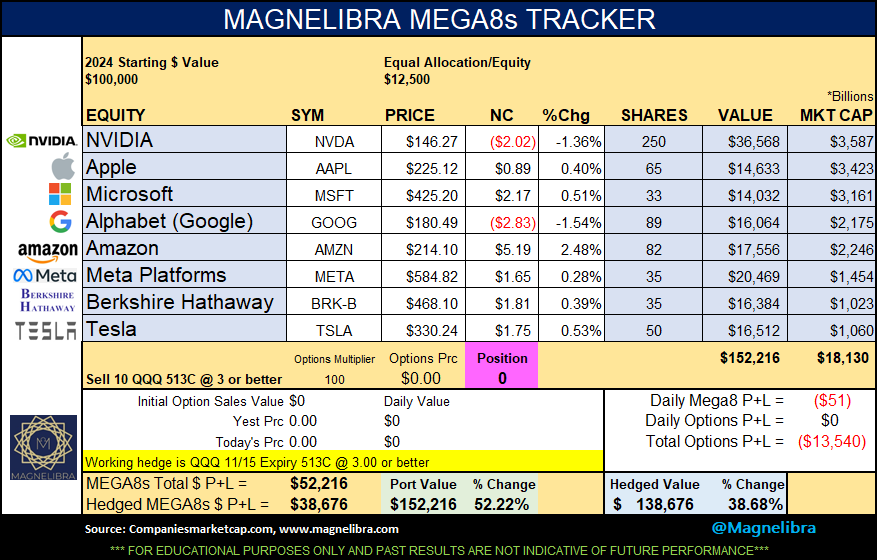

Ok onto the settlements and the MEGA8s:

As far as the MEGA8s they hit $18.13Tn in market cap yesterday with Amazon the continued leader for now. As far as the hedge for this week, it moves to hedge with the 513C at 3.00 or better. For now that hedge is far away, but its only a guide to what can be put on. We suspect we will start to look at next weeks options and probably target the 515 call for $4.50 or better so keep an eye on that, we may update later today with that one that expires on 11/22 all for your educational learning of course and always make sure you understand your own risk reward profiles:

As far as the settlements, you can see that the shorter end of the bond markets are gaining as the longer end falls off, this is the expected route for the start of this rate cut cycle. Equities had a pretty muted day overall, Bitcoin above 90k, continued dollar strength and energies up slightly with Metals continuing downward:

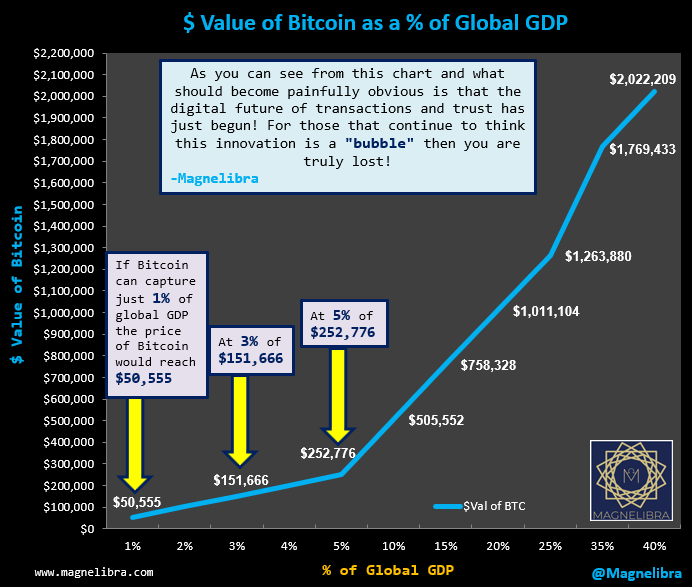

Speaking of Bitcoin, we have a chart if you missed it but it is truly what the expected path will be if we continue to expect global GDP transacted in Bitcoin to grow. We first put this chart out some 7 or 8 years ago, so we were way ahead of the pack, any long time followers know this and quite often we took a lot of crap in those early years and post the 2017 meltdown, but none the less, we are confident over time that BTC will capture GDP. It is by far the best definition of money as described as absolute scarcity! So anytime anyone ever questions your loyalty to Bitcoin, give them this chart and tell them to shut up, you don’t care about the short term price of it, you are looking 10, 20 years and beyond!

Ok guys this is a good place to end it, oh wait, I saw this chart of CAVA and couldn’t help but make an opinion. I know my kids like this place, but they don’t like it that much…so looking at the chart, well, lets just say, it could be time for some Put structures:

The April 17th expiration $120/$90 put spread can be bought for $5.70 and max profit would be $30. That is a risk/reward structure of 5.2x. I just thought I would toss that out there. I like the same idea in Nvidia because of what’s going on with SMCI! So for Nvidia the same expiration put structure is $4.88 ( $120put is 6.50 and $90put is 1.62) this one is a better payoff value at 6.1x!

Anyway, those are my thoughts today, we are glad we did this podcast style today because we feel many would rather listen than read, I may eventually start doing videos but would need to figure out which software might be best for that! Anyway please subscribe, like, share or do whatever it takes to help spread the word. We are providing knowledge like no other here and we hope it entices you to generate new and unconventional thoughts in your own world. That is the key to success!