Yield Curve, Settles Data GFBP & More

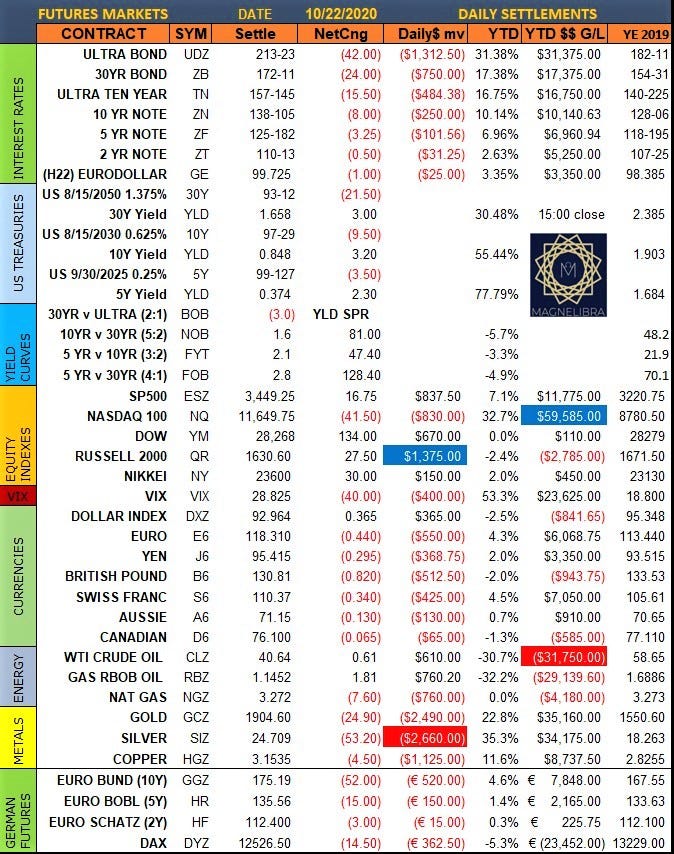

Let’s start this letter off with yesterday’s settlement picture. For those new to the letter, this is the settlement sheet that Magnelibra Econemotions uses to track the various markets and sectors that Magnelibra Capital Advisors the CTA follows. We like to look at prices but more importantly we follow the money flows in terms of actual dollar cost. We feel this paints a better picture in some cases and offers a different vantage point and additional data points opposed to just focusing on static prices:

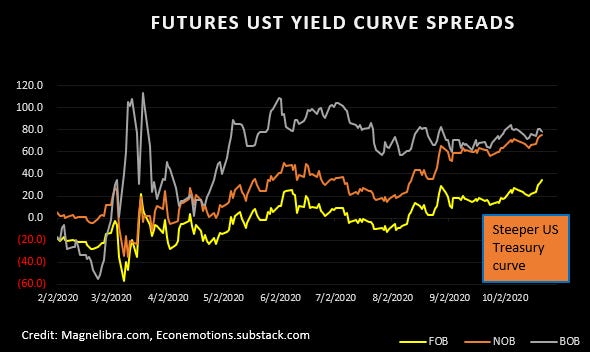

With the yield curves steepening out and all this talk of YCC (Yield Curve Control) it will be interesting to see how the FED will handle any real spike in yields. We posted about that 10Y options strangle the other day which highlighted the 0.65% to 1.00% zone and we feel that’s about the scope of the entire value area the FED will most likely want to try and control things within.

However we must note as debt levels increase and balance sheets increase ($7.1T and counting FED Assets), things get a lot more complicated and tools that once worked will no longer work. Well, at least not in the way the 700 PHD economists at the FED think they will work. We have always had this disdain for academic prowess vs actual practitioner (Trader/investor) whom the latter operates not in a vacuum but in the real world where real dollars, euros and yen are made and lost.

Anyway the 10Y US Govt yield hit 0.848% and technically this area is pretty significant, but for us makes a bit of sense given the election uncertainty as well as the November refunding. The longer term trend line is denoted above in the pink/purple line:

Looking at how much the curve has steepened since the yields began rising, let’s look at our proprietary futures curve chart, where the 5s30 has led the way:

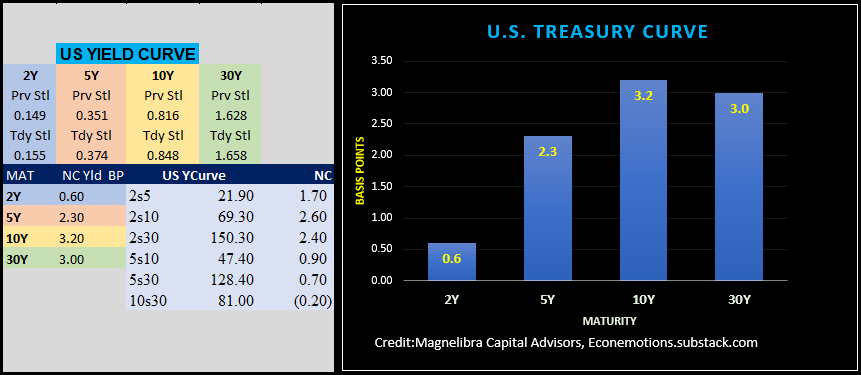

Here is a bit more granular US Govt Yield Curve data that we follow:

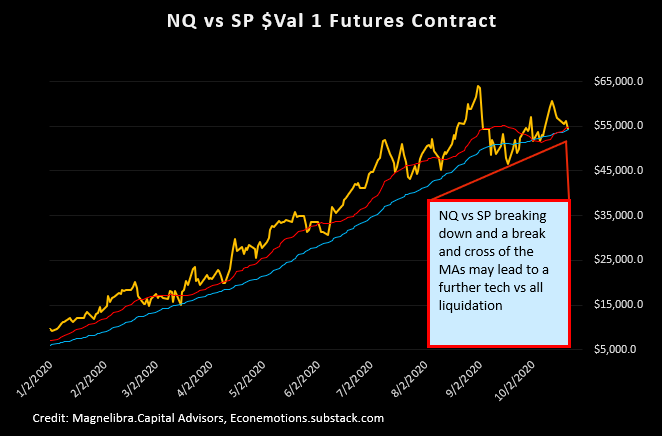

Moving along to the Equities, where Magnelibra Econemotions has been highlighting the volatility in the indexes vs one another, in particular the Nasdaq vs the SP500, yes we know where everyone is hiding and we know all the capital is concentrated in just a few names. Yes you can throw out diversification because all roads are leading to the same tech warehouses, clouds, servers, informational databases, streamers, whatever your fancy. Anyway here is another proprietary Magnelibra chart and its just another reference propelling Magnelibra’s dislike of the Nasdaq vs the other Indexes. This chart is a contract value to contract value total return:

As far as the other settles, we know the US Dollar Index has been hammering it out near the 93.00 level and that the Euro has had a rough time breaking away from the 118 handle. All in all its a mixed Brexit bag in FX land, but we will suspect the academic crowd to continue to push for a weaker dollar, yet we just don’t buy it, not yet at least.

Energies have been battling the Covid demand shock and continue to be stuck near $40. This is much better for the bull case than the $36 area where the bulls stepped in to support, but $42 is the next hurdle and it doesn’t seem we will be breaking those ranges anytime soon here.

Gold and Silver running around $1900 and $25 respectively. Magnelibra Econemotions continues to favor Gold over Silver here especially with Silver still below the $26 hurdle rate its seems.

Finally we saw this headline out from Forbes:

PayPal Just Gave 346 Million People A New Way To Buy Bitcoin—But There’s A Nasty Catch

Yea there is a catch alright and its something we truly believe in as well as Bitcoin the technology was designed to eliminate 3rd party attribute and risks and to quote Satoshi Labs, the creators of cryptocurrency hardware wallet Trezor,

"Not your keys; not your coins"

Yes that is the correct way to look at the technology, sure by allowing digital currencies PayPal expands the ecosystem of Cryptocurrencies but in no way does it invoke the original utility the technology was designed for. (P2P, immutable, trustless, decentralized system) All in all it has boosted Bitcoin though, here is our latest chart on it where we highlighted 2 weeks ago the potential triangle breakout and now look at it:

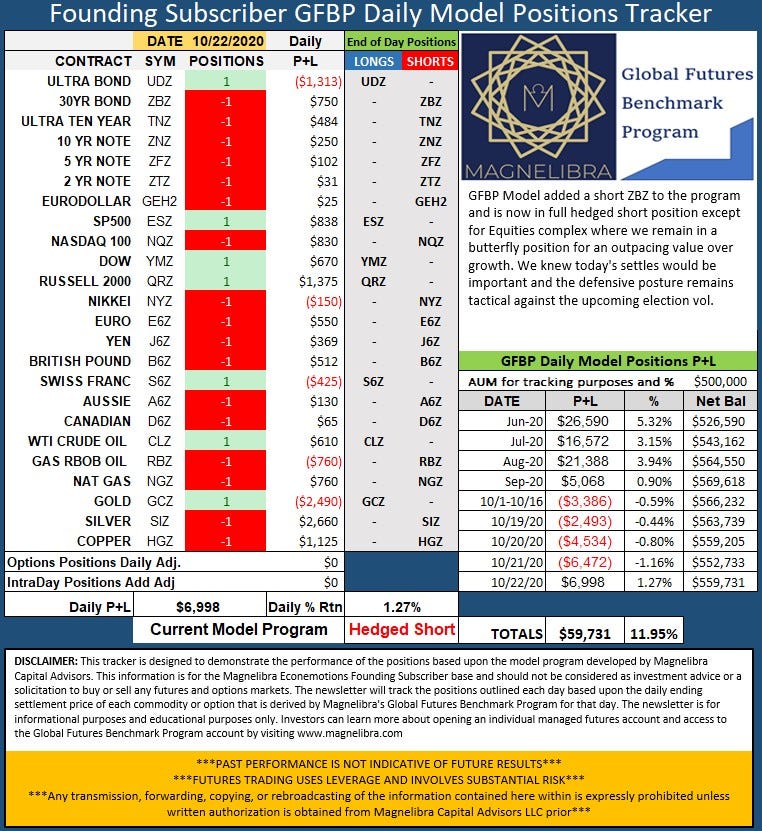

Finally for those interested in following our Global Futures Benchmark Program Positions Tracker where we highlight the Magnelibra CTA program proxy indicators for the markets we follow, here is a glimpse of the recent positioning and performance. The Positions Tracker has been in a defensive Hedged Short mode for awhile and we are continuing on with it presently:

Founding Subscribers get access to this proxy positions tracker and as a newsletter its P+L is derived from the daily positioning that the proxy program has on as indicated. Generally new or removal of positions are noted and adjusted for pricing and if there are options positions on as well they will be denoted in the adjustment area so that we can be as transparent as possible as to the tracker, its position sentiment and how one would have performed if they followed along. Our hope is to give investors/traders a better look how Magnelibra Econemotions is looking at each market segment and give you more insight as to how we are viewing things. Our goal is to grow this newsletter into a tool not just for investors, but for those wanting to better grasp and understand the financial system that we are confined in.

Ok that’s it good luck today! If you think this offers value, let us know, if you think were full of it let us know, if you think we could do more, let us know, there are no limits as to where we can take this and if you have suggestions, let them fly!

Please share our work and subscribe if you haven’t already, we have a free tier, a 2 latte a month style and a Founders which has access to our Global Futures Benchmark Program positions tracker daily. We hope you enjoy our work and we hope you continue to support us.

-Magnelibra Econemotions

DISCLAIMER: For educational purposes only. This is not a solicitation to buy or sell commodity futures or options on neither commodity futures. The risk of trading securities, futures and options can be substantial and is not for everyone. Such investments may not be appropriate for the recipient. The valuation of futures and options may fluctuate, and, as a result, clients may lose more than their original investment. Nothing contained in this message may be construed as an express or an implied promise, guarantee or implication by, of, or from the author Michael Agne owner of Magnelibra Capital Advisors. All rights are reserved. We will never claim that you will profit or that losses can or will be limited in any manner whatsoever. Past performance is not necessarily indicative of future results. Although care has been taken to assure the accuracy, completeness and reliability of the information contained herein, we make no warranty, express or implied, or assume any legal liability or responsibility for the accuracy, completeness, reliability or usefulness of any information, product, service or process disclosed.